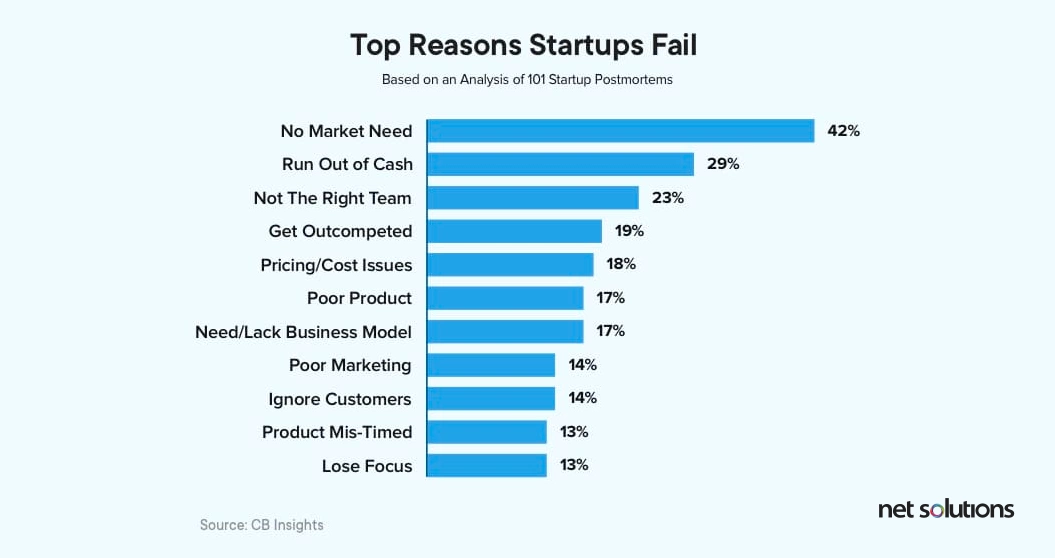

Launching a startup is about more than just making money; it's about introducing innovative ideas that can improve lives. However, a staggering 90% of startups fail due to a lack of market demand, incompetence, or lack of experience. Success requires not only a brilliant concept but also the knowledge and skills to navigate the startup landscape effectively. In this blog, we'll explore startups, types, and strategies for success.

A startup is the early stage of a company, usually founded by entrepreneurs with a vision to create a product or service to meet market needs. Innovation is key as startups aim to improve existing products or introduce new ones. Their main goal is often to grow the venture for a profitable sale or to go public through an IPO (Initial Public Offering, is a way for a private company to become public by selling its shares on a stock exchange).

Types of startups:

Scalable startups.

Tech startups, prominent in the industry, possess significant global potential. Given their technological edge, they seamlessly penetrate international markets with backing from investors.

Small business startups.

Small businesses, initiated by individuals, typically rely on self-funding for growth. They progress steadily, often boasting physical storefronts but lacking online presence. Examples abound in local establishments like grocery stores, hair salons, bakeries, and travel agencies.

Lifestyle startups.

Emerge from individuals passionate about their hobbies, aiming to turn them into profitable ventures. These entrepreneurs find fulfillment by monetizing their passions, such as dancers who establish online dance schools to teach both children and adults. Through these endeavors, they not only pursue their interests but also generate income.

Buyable startups.

In the technology and software sector, there's a niche of startups designed specifically for acquisition by larger corporations. Entrepreneurs create these startups with the intention of selling them to bigger players like Mahindra or Tata. These giants acquire these smaller startups to further develop them and reap the rewards of their growth and innovation.

Big business startups.

Dominant players in the market, these companies begin with innovative and scalable concepts. Their aim is clear: to outshine competitors in the industry. Pursuing high growth and profitability, they exemplify the scalable startup model. Google and Facebook stand out as prime examples, both starting with the ambition to assert their dominance in their respective fields, a goal they achieved with resounding success.

Social startups.

They emerge with a mission to address societal, cultural, or environmental challenges, aiming to bring about positive change rather than solely seeking profit. Driven by a passion for making a difference, social entrepreneurs dedicate themselves to improving the lives of marginalized individuals. They adeptly identify and tackle social, financial, and environmental issues. Take, for instance, the Aravind Eye Care System, an Indian social enterprise employing a cross-subsidy approach to deliver accessible eye care services. Through this model, paying patients help subsidize treatment costs for those in need, exemplifying the impactful work of social startups.

Tips for Making a Successful Startup

Achieving success in the world of startups is far from swift or guaranteed. The journey is often marked by unpredictability and occasional chaos. Wondering how to embark on this adventure? We've curated some valuable insights on launching a new startup venture.

1. Define the Target Audience

Identifying your target audience is crucial for your startup as it allows you to tailor effective marketing strategies. By honing in on potential customers, marketers can optimize their efforts and resources. Understanding your target audience streamlines marketing campaigns, making them more cost-effective. When you've thoroughly analyzed and catered to this segment, you'll achieve the highest conversion rates for your business.

Tips for finding your target audience:

- Start with broad assumptions

- Narrow down the audience

- Analyze your business competitors’ target audiences

- Conduct research on the supposed audiences

- Choose the audiences that are most likely to buy your product

- Conduct interviews

- Draft your ideal client portraits

- Refine your portraits

2. Less Spending

When contemplating startup creation, budget constraints are often top of mind. It's essential to be mindful of finances. Overspending on broad audience targeting can lead to significant budgetary setbacks. So, how can companies and potential investors circumvent this risk? Firstly, aspiring entrepreneurs should pinpoint potential investors for their business. Attempting to target everyone with a limited budget hinders effective audience engagement via ads, emails, etc., thus impeding lead conversion.

Narrowing down the target audience and engaging with them effectively can significantly boost lead generation.

3. Create Ideal Customer Profile (ICP)

An Ideal Client Profile (ICP) strengthens a company's sales strategy by focusing solely on prospects most likely to benefit from its offerings. This profile includes key statistical data like technographics and firmographics.

Technographics refers to the analysis of the technological characteristics and behaviors of individuals or organizations. It involves understanding aspects such as the software, tools, and technologies they use.

Firmographics, on the other hand, is similar to demographics but focuses on businesses rather than individuals. It involves collecting and analyzing data about a company's size, industry, revenue, location, and other relevant characteristics.

4. Identify the audience's pain points & provide solutions through your product.

It's essential to recognize that every new venture must address a market need or problem. While finding a solution to the problem is crucial, articulating the problem itself can be challenging. To help navigate this process, it's important to craft clear problem statements.

Here are some tips for creating effective problem statements:

- Identify your target market.

- Focus on defining one specific problem.

- Be precise about what the problem entails.

- Understand the pain points associated with the problem.

- Define a practical solution.

5. Identify Your Competitors

Understanding your competition is crucial for any startup.

Here's why analyzing competitors is essential:

Differentiation: By identifying competitors' strengths and weaknesses, you can develop a Unique Value Proposition (UVP) to set your startup apart.

Audience Targeting: Analyzing competitors helps you determine whether to target the same audience or explore untapped markets.

Marketing Channels: Researching competitors can reveal new marketing channels and industry trends.

Product Analysis: Studying competitors' products allows you to benchmark and refine your own offerings.

It's important to research both direct and indirect competitors. Direct competitors offer similar solutions to your target audience, while indirect competitors operate in the same industry but may offer different products or services.

Here are effective ways to research competitors:

Utilize search engines: Explore competitors' websites, articles, press releases, and social media presence to gain insights.

Employ analytical tools: Tools can provide valuable data on competitors' SEO, web traffic, PPC ads, blog posts, and social media activity

Conduct client interviews: Reach out to former clients of competitors to gather first hand feedback and understand customer concerns.

6. Develop a Unique Value Proposition

A Unique Value Proposition (UVP) is a concise statement that communicates the relevance, value, and differentiation of your product from competitors. Your UVP may be embedded in your product features or the concept of your new startup. It's essential to craft a memorable slogan or motto based on your UVP to inspire users.

Here are steps for creating a compelling UVP for your startup:

Understand your customer: Conduct thorough research and interviews to gain insight into your target audience's needs and preferences.

Draft your UVP: Keep it concise and focused, ideally between 10 to 30 words. Highlight the main benefit(s) for the customer, followed by any additional benefits related to price, quality, service, etc.

Ensure your UVP sets you apart from competitors, making it truly unique.

7. Define your startup's monetization model

Defining your startup's monetization model early on is crucial. Researching competitors' strategies can provide valuable insights. Consider pros and cons of various models and leverage your unique approach to stand out.

Here are top monetization models:

Subscription Model: Customers pay a recurring fee (monthly or annually) for access to a product or service. Benefits include predictable revenue and customer loyalty, but continuous value delivery is required. Ideal for SaaS, streaming platforms, and subscription boxes.

Freemium Model: Offers basic services for free with premium features available for purchase. Facilitates user acquisition and potential for a large user base, but converting free users to paid can be difficult. Suited for digital products like apps, software, or online platforms.

Advertising-Based Model: Generates revenue by displaying ads to users, keeping the service free. Scalable and ideal for platforms with large user bases. However, ads can impact user experience and revenue relies on high traffic. Suited for media sites, social networks, or platforms with high user engagement.

Transaction Fee Model: Charges a commission for each transaction processed through the platform. Customers appreciate the direct fee for transaction volume, but high transaction volume is needed for profitability. Commonly used in E-commerce platforms, payment gateways, or marketplaces.

Licensing Model: Users pay for permission to use intellectual property or software, akin to a subscription model. Offers consistent revenue and high profit margins, but relies on strong Intellectual Property (IP) or unique software.

Vulnerable to piracy. Commonly used by software providers, media companies, or businesses with proprietary technologies.

8. Think before bootstrapping

Bootstrapping, or self-funding, involves using personal resources to grow your company rather than seeking outside investment like angels, venture capital, or friends and family. While it offers several benefits such as full ownership, greater control, and limited debt, there are also drawbacks to consider.

Pros:

Full ownership: Bootstrapping allows founders to retain complete ownership of their company, ensuring they receive 100% of the profits.

Greater control: Without external investors to answer to, founders have more control over the direction and decisions of their company.

Limited debt: Bootstrapped businesses typically rely on personal savings or initial income, minimizing the risk of accumulating substantial debt.

Cons:

Financial risk: Founders bear the direct financial risk of the business, potentially impacting personal finances if the company encounters difficulties.

Less credibility: Without external backing, bootstrapped businesses may face challenges in building credibility and establishing connections within the industry.

Slower growth: Bootstrapped companies often experience slower growth due to limited resources for marketing and expansion, and may struggle to meet increasing demand.

9. About raising funds to your startup

Raising funds enables a business to acquire capital without incurring debt. This can be achieved through investments, known as equity financing, where investors provide capital in exchange for ownership stake in the business. Another option is crowdfunding.

Investors: Investors can be individuals you know, such as friends, relatives, or colleagues, or they could be venture capitalists. Venture capitalists specialize in funding early-stage startups with high-risk but high potential.

Friends and Family : When seeking funding from friends and family, it's important to establish written agreements outlining the terms of the loan.

Venture Capital: Venture capital can be provided by wealthy individuals, known as angel investors, or venture capital firms. These investors often have specific investment criteria and may provide guidance to the startup founders.

Crowdfunding: Crowdfunding involves raising small amounts of money from a large number of people to fund a project or business. Campaigns set a fundraising goal and timeframe, and sharing the campaign helps raise funds and create awareness. Many crowdfunding platforms exist, so it's essential to research fees and campaign rules to maximize fundraising efforts. Crowdfunding can also involve selling small amounts of equity to multiple investors to fund a company.

Pros and Cons of fundraising your startup.

Pros:

Cashflow: Investors provide essential capital to sustain and grow your business operations. Their investment demonstrates a vested interest in your success, fostering a lasting relationship that can support your business throughout its journey.

Expertise and connections: Beyond financial support, investors offer valuable expertise and networking opportunities. Their experience and connections can open doors to strategic partnerships, suppliers,distributors, and customers, enhancing your business's prospects for success.

Faster growth: With financial backing from investors, achieving success and expansion becomes more attainable. Access to additional resources and industry insights enables you to make impactful business decisions, accelerating growth opportunities like product expansion or market reach.

Cons:

Less control:Taking on investors often means relinquishing some degree of control over your business. Investors may have differing ideas and expectations, potentially conflicting with your long-term vision and decision-making autonomy.

More pressure to make a profit: Investors expect a return on their investment, increasing the pressure to generate profits and deliver regular performance updates. Meeting investor expectations may require prioritizing profitability over other business objectives.

Potentially less profit:Sharing profits with investors reduces the amount of earnings retained by the business owner. Whether through equity stakes or repayment with interest, investor financing can diminish overall profitability for the business. Considering these pros and cons can guide your decision on whether to pursue investor funding. The trade-off lies between accelerated business growth and potential loss of control. While investors can offer invaluable support and opportunities, their involvement may also diverge from your original business vision. Ultimately, the choice depends on your business principles and the perceived value of success.

10. Build a Minimum Viable Product (MVP)

An MVP, or Minimum Viable Product, is a simplified version of a product containing essential features that define its value proposition. It aims to expedite time to market, engage early adopters, and attain product-market fit swiftly. The MVP concept emphasizes delivering the minimum essentials to satisfy initial customers, followed by gathering feedback for future product iterations.

Crafting an MVP is a proven strategy for innovative product development, embraced by industry giants like Dropbox, Figma, and Uber. Rather than rushing into coding, prioritize creating an MVP to validate market demand. Define your narrative, highlight uniqueness, and identify the value proposition and problem you aim to solve.

11. Do Not Put Off Marketing

When initiating a startup, marketing expenses are often overlooked, despite their potential to match or surpass the cost of creating the startup. It's wise to craft a marketing plan early in the startup development process, outlining budgets for both initial growth and ongoing promotion of the product or startup.

Other Important Points to Consider Before Launching a Startup

Audience Segmentation: Engage with at least 100 potential clients to understand their preferences, pain points, and buying behaviors.

Competitive Intelligence: Conduct a thorough review of competitors' strategies to identify market gaps and refine your value proposition.

Market Validation:

-

Social Media Analytics: Monitor trends and feedback on platforms like Instagram, Facebook, and LinkedIn.

-

Industry Reports: Analyze data-driven insights to understand market dynamics. c. Stakeholder Interviews: Gather qualitative feedback from potential clients through interviews.

Feasibility Assessment: Ensure there's tangible market demand for your concept by conducting rigorous analysis and adjusting strategies accordingly. Adaptability is key for startups to thrive amidst changing customer needs, technological advancements, and global trends. Successful founders can quickly adapt to market feedback and adjust their strategies accordingly.

Networking is essential for business growth as it facilitates mentorship, collaboration opportunities, and referrals from peers and industry experts.

Legal preparedness is crucial for financial integrity and risk management. Understanding relevant laws, obtaining licenses, and maintaining compliance are vital aspects of building a strong legal foundation.

Prioritizing client relations is essential for building brand loyalty and reputation.

Consistently delivering exceptional customer service and addressing customer feedback are key strategies for ensuring customer satisfaction and fostering brand advocacy.

By prioritizing these pillars, entrepreneurs can navigate the complexities of the business landscape with confidence and resilience.

Most common challenges faced by startups

Facing challenges is inherent to the competitive landscape of the corporate world, particularly for startups. Here are some key hurdles they encounter:

Intense Competition: Startup businesses face fierce competition, especially in the online sphere, necessitating aggressive strategies to stand out.

Unrealistic Expectations: Achieving success can lead to unrealistic expectations, emphasizing the importance of sustainability and controlled growth.

Hiring Suitable Candidates: Building a cohesive team is crucial, but identifying and hiring suitable candidates is challenging in today's digital age.

Partnership Decision Making: Startups struggle to find trustworthy partners, especially in the tech sector, requiring careful consideration before collaborating.

Financial Management:Managing finances becomes increasingly complex as startups grow, requiring prudent decisions and possibly external financial consultancy.

Cyber Security: With the rise of cyber threats, startups, particularly those operating online, must prioritize robust security measures to protect sensitive information.

Winning Customer Trust: Customer trust is paramount for startup success, necessitating a customer-centric approach and proactive efforts to build loyalty.

Overcoming these challenges requires resilience, integrity, and adaptability. While there's no one-size-fits-all solution, startups can navigate these hurdles by remaining steadfast and open to innovative strategies.

12. Five Growth-Hacking strategies for startups

Growth hacking involves utilizing cost-effective methods to rapidly expand a company's reach and achieve profitability, making it particularly appealing to startups with limited resources. Beyond just financial benefits, high growth rates enable startups to secure early customers, gain media visibility, and build trust with their audience.

Despite budget constraints, growth hacking empowers new businesses to achieve exponential growth through innovative strategies. This approach levels the playing field, allowing all startups to scale rapidly with a bit of creativity.

Here are five growth-hacking strategies to consider:

Referral/Affiliate Program: Encourage satisfied customers to share their positive experiences with others in their network by rewarding them for successful referrals. Influencer programs can also be effective, incentivizing individuals to promote and sell on your behalf.

Partnerships: Collaborate with non-competitive companies that share your target market to leverage each other's audiences and marketing resources. This can amplify your impact and reach at minimal cost.

Contests: Engage potential customers through competitive contests, incentivizing participation with valuable rewards. Encourage entrants to share the contest with others to maximize exposure and potential virality.

Free Downloadable Content: Offer valuable content gated behind email sign-ups or other contact information. Providing relevant and insightful content can attract leads and qualify potential customers.

Free Trials: Allow potential customers to sample your product or service for free to showcase its benefits and value. Freemium models can entice users with limited features, eventually upselling them to paid versions.

While not every growth-hacking endeavor may yield explosive results, it's essential to measure and monitor outcomes to identify successful strategies and pivot quickly from unsuccessful ones. Implementing these strategies as ongoing experiments within your marketing team can help allocate resources effectively while continuing regular marketing practices for steady growth.

13. Startup scaling strategies

There is no single way of scaling up your business. There are many different strategies you can choose from.

Moving to the next round of funding is a crucial step for startups following the traditional funding path. Preparation involves creating a compelling pitch deck and organizing financial statements and related documentation. Expect tough questions from investors and be transparent about expansion plans, profitability, and return on investment timelines.

Investing in technology is another effective strategy for scaling up a startup. Enhancing current technology or transitioning to a more modern IT infrastructure can improve customer service and handle increased user traffic.

Implementing a new marketing strategy can significantly boost business growth. Creating impactful marketing campaigns, leveraging social media, and exploring various marketing channels can attract more customers and increase sales.

Launching complementary products or services can expand business offerings and attract new customers. Investing in product development to meet customer needs can drive growth and increase market appeal.

Reflecting on current processes and streamlining inefficient practices can optimize business operations and fuel growth. Automation and efficiency improvements can save time and resources, enabling faster scalability.

Hiring experienced management professionals can bring valuable expertise and perspective to the startup. Experienced managers can handle stressful situations, improve organizational structure, and retain top talent, ultimately driving business growth.

Building a business that can run without sole dependence on the founder is essential for long-term success. Distributing roles and responsibilities across the company, hiring specialized talent, and relinquishing control can increase agility and resilience to market changes.

Startup India

Launched on January 16, 2016, the Startup India initiative aims to establish a robust and inclusive ecosystem for entrepreneurship in India, fostering startups and innovation. The initiative seeks to empower startups to expand and disrupt through technology and design, while also generating employment opportunities and driving economic growth. Managed by a skilled team reporting to the Department for Industrial Policy and Promotion (DPIIT), the scheme offers numerous benefits to entrepreneurs across the nation.

Benefits of the Startup India Scheme:

- Simplified Process and Support

- Easy registration process with support from the Startup India team at every stage

- Legal support at reduced costs for startups

- Relaxed norms for public procurement process

- Launch of portal and mobile app for information exchange and compliance

Eligibility Criteria for the Startup India Scheme:

- To be recognized as a DPIIT startup, companies must meet the following parameters

- Existence period of the startup should not exceed 10 years from the date of incorporation

- The company must be a Limited Liability Partnership (LLP), Registered Partnership Firm, or a Private Limited Company

- Annual turnover should not exceed ₹100 Crores during any financial year since inception

- The original business entity should not have been established by reconstructing an existing business

- The startup must work towards improving or developing a certain product or service

- Support a scalable business model demonstrating high potential for employment generation and wealth accumulation

Documents Required for the Startup India Scheme:

To register your startup, submit the following documents:

- Certificate of Registration or Incorporation

- PAN card of the company

- Proof of concept (website link or video)

- Proof of funding (if applicable)

- List of recognitions and awards

- Authorisation letter from the authorized company representative

- Certificate of incorporation

- MSME registration, GST registration, Trademark registration certificates (if available)

- Company’s website or profile

- Details of company directors

- Revenue details

Startup India Registration Process:

Follow this process to register your enterprise under the Startup India Scheme:

- Incorporate your business as an LLP, partnership firm, or private limited company

- Register the business on the Shram Suvidha portal

- Enter your details and upload supporting documents

- DPIIT verifies your information and grants approval if you meet eligibility terms

Tax Exemptions Under the Startup India Scheme:

All startups registered under this initiative are eligible for tax exemptions under Section 80IAC and Section 56:

- Tax exemption for a maximum of 3 consecutive financial years within the first 10 years of inception

- Exemption for investments exceeding ₹100 Crores from listed public entities with a net value or turnover exceeding specified limits

- Shares from startups up to a maximum limit of ₹25 Crores included within the tax exemption threshold limit

Entrepreneurship offers both excitement and challenges. Stay resilient, innovative, and adaptable as you navigate the journey of starting and growing a business. Embrace setbacks as opportunities for growth and surround yourself with a supportive network of mentors and peers. Remember, success is about the journey as much as the destination. Stay focused, determined, and inspired, and make your mark on the world.

.jpg)